One of the most overlooked yet troubling aspects of Biden’s plan is his doubling of the Global Intangible Low-Taxed Income (GILTI) tax. GILTI taxes items that generate foreign income and profits owned by American companies with foreign affiliates. This is troubling, because GILTI taxes American companies on income that has virtually nothing to do with anything in the United States. It’s bad enough that the current tax rate is 10.5%; Biden wants to raise this to 21%.

The tax laws of every developed country – except the US – provide that their companies do not pay tax on earnings from outside their country. Thus a German company earning money from activities in China or the UK pay taxes only to that jurisdiction – not to Germany. The US always taxed US companies on earnings from abroad, as soon as that money was returned to the US. That created a pretty stupid situation, encouraging these companies to leave this money outside of the US, and invest it in foreign, non US ventures.

The GILTI tax was created as part of the Tax Cuts and Jobs Act (“TCJA”) of 2017 as part of the attempt to fix this situation. What the TCJA did was require that all companies with foreign operations have to pay a penalty tax on all the money accumulated abroad, going back to the ‘80s; this rate was low and spread over 8 years. In exchange for it, the idea was that US companies would now be on par with other countries, in a territorial formation. In other words, pay a low tax on the money the US company never repatriated, repatriate it, and then in the future, you don’t pay tax on it, thereby discouraging profit shifting.

But Congress lied. In addition to paying the upfront tax at a low rate and thereby getting a tax for the future, they couldn’t help themselves. They added the GILTI tax, so now it’s taxed whether it’s repatriated or not. And this is bad. Congress reneged a little bit, because the GILTI is a relatively low tax but because it is worldwide, and now they have to pay tax every year on these foreign profits. So companies paid upfront and now they have to pay this tax every year — albeit at a low rate — so now it’s worse.

Now what Biden is suggesting with the GILTI tax is basically fraudulent. People paid that upfront fee so not to have to pay taxes — and now with this proposed 21% rate — is like fraud against American international companies. The 2017 tax act required an upfront benefit that got future benefits, now Biden wants to take away the future benefits.

GILTI puts American companies operating abroad at a competitive disadvantage. The foreign affiliates already have to pay a penalty tax just to be on equivalent footing with other companies abroad (companies that don’t have to pay the GILTI tax here, mind you). GILTI then tacked on a 10.5% tax and now Biden wants to double it — when it should be ZERO.

Biden’s plan to double GILTI goes hand-in-hand with his overall plan to tax U.S. businesses (he also wants to raise the corporate tax rate to 28% and add a 15% minimum tax based on profit reported on financial statements.) Going after businesses is already bad policy and his desire to double GILTI shows his ignorance and his willingness to further erode American competitiveness.

The amount of money Biden’s plan will raise is relatively insignificant (roughly $300 billion over the next ten years) but his attack on businesses is mean-spirited; it hurts our country by making our domestic companies less able to compete abroad in foreign markets. Nevermind that foreign income shouldn’t even be taxed at all! How can Biden justify raising taxes in a way that will make the United States less competitive and will reduce jobs? Increased taxes are a disincentive towards investing and job creation and will only hurt our economy.

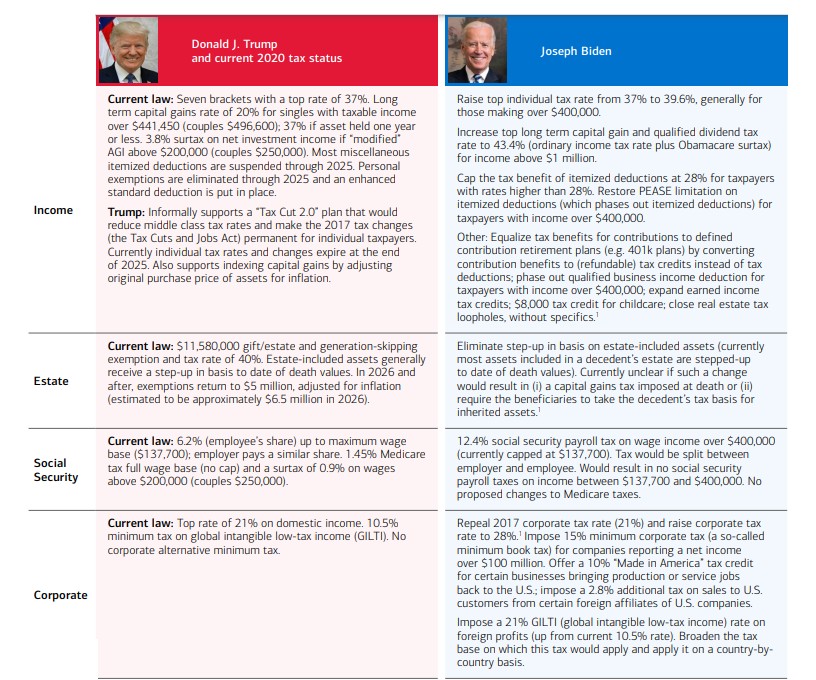

Now that Biden has been elected President, it’s important to take stock of what tax changes are likely to be coming. Merrill Lynch did a good job putting together a side-by-side comparison of current tax law in four areas: income, estate, social security, and corporate, and then possible changes in those areas according to Biden’s campaign tax plans. The summary is below.

It is notable that in just about every instance, there will be a tax increase under Biden’s plans. How this will impact the economy, jobs, wages, and investments remains to be seen.

Earlier this year, California passed AB5, a measure that would require companies to reclassify independent contractors as employees. The problem is that the government is yet again intruding on employer-employee relationships under the guise of worker protections. Furthermore, it’s an attempt to put unions even more in charge of things in California while also purporting to provide more revenue to a nearly-bankrupt state, all doomed to failure because of its economic ignorance.

AB5 affects those workers who belong to the gig economy. “Gig economy” is the catchphrase for the portion of the economy made up of freelancers and independent consultants. It’s estimated that 1 in 3 workers now, about 55 million, fall into this category. The gig economy has grown to be very good because it provides much-needed work flexibility and independence that many workers prioritize.

The mechanism by which freelance workers are deemed employees is the “ABC test.” This is the court created formula that companies must apply in order to determine if workers are contractors instead of employees, and it puts the burden of proof on employers. A worker is a contractor if he meets the following three criteria:

1) The worker is free from the control and direction of the hiring entity in connection with the work’s performance, both under the contract for the performance of the work and in fact.

2) The worker performs work that is outside the usual course of the hiring entity’s business.

3) The worker is customarily engaged in an independently established trade, occupation, or business of the same nature as the work performed

There is no economic or business rationale to these tests – they were created solely to destroy the concept of independent contractor by making virtually all relationships that of employer/employee. The IRS, on the other hand, has established criteria for what constitutes a real employee based on behavioral control, financial control and relationship of the parties. It should also be noted that if the IRS follows the AB5 definition of employee for Californians, the employees will be devastated! That is because under IRS tax rules, employees may not deduct any business expenses, which is a critical tax benefit to the independent contractor relationship.

It is particularly frustrating that advocates of AB5 purposefully ignore the fact that the gig economy arose during the weak Obama economy, which was littered with ever-increasing government regulations and crushing legislation such as Obamacare. This combination made it difficult to become a business or stay in business. It was certainly no wonder that businesses sought alternative forms of employer-employee relationships, which is their inherent right to do so. AB5 now undermines those relationships.

Furthermore, AB5 essentially picks winners and losers; large swaths of independent contractors are exempt, while others have restrictions, and still others are not exempt at all. Among those exempt include: “insurance brokers, doctors, dentists, lawyers, architects, engineers, private investigators, accountants, investment agents, salespeople, commercial fishermen, and real estate agents.” Among those partially exempt include journalists and freelance media-makers such as photographers, but they are now limited in their number of contributions to 35 items per year. Those industries not exempt at all include Uber and Lyft, companies who successfully arose as alternative transportation options during the rise of the gig economy.

And yet, there are really no winners here. Certain industries are exempt, but there’s no justification to do that from a logical point of view. The sole reason why some have an exemption is because they have too strong of a lobby or union presence — which is an irrational justification. There will also be a never-ending succession of lawsuits, as workers try to avoid being treated as an employee. The only winners will be the lawyers.

The gig economy has proven to be a resourceful alternative for workers who seek a myriad of benefits, including work independence, flexible schedules, side money, and increased quality of work-life balance. Now that the economy has recovered from the anemic and over-regulated Obama years, governments such as California are happy to cash in on its success while strangling its workers and businesses with unnecessary, burdensome measures. AB5 will ultimately weaken the economy and destroy some businesses in its wake.

On November 3, Illinois residents have a Constitutional referendum to change their method of taxation from a flat tax to a “fair tax.” The current system treats all Illinois taxpayers the same by levying a modest 4.95% rate. Under the proposed change, taxpayers would be divided among multiple tiers with a progression of increased rates based on higher levels of income, and both individual and corporate rates would be affected. By removing the Constitutional provision against graduated-rate taxes, the power of taxation is given to the state lawmakers who can decide varying levels of rates for various groups of taxpayers with a simple majority vote. In contrast, the flat tax provides some protection against outrageously high rates because it is impractical and politically unpopular to do so among certain segments of the population.

In anticipation of the referendum passing, the Illinois legislature passed a tax plan that would be implemented on January 1, 2021. Although the Illinois governor — like most progressive morons — has assured taxpayers that the change won’t affect most residents, the impact of the new plan will indeed have dire consequences for many individuals. The new tax rates range from 4.75% to 7.99%. While the lowest 20% of earners will see a decrease in rates, that translates into a whopping $6.00 on the median average earnings of $12,400. On the other end of the spectrum, the new plan includes not only higher rates, but also a recapture provision for highest earners, so that not just their marginal income, but their entire income, is taxed at the 7.99% rate. What’s more, the new plan does not index for inflation on marginal income levels which will result in taxes consuming a greater percentage of taxpayer income if income levels do not increase.

Businesses will also be adversely impacted. The base corporate rate will increase to 7.99%. However, Illinois also has an additional set of taxes (called the PPRT) levied on corporate and pass-through income of 2.5% and 1.5% respectively. Combined with the new business rate, corporate income tax would be 10.49% and pass-through income tax would be 9.49%. At a time when businesses are struggling due to the pandemic, increased taxes only worsen the situation. Additionally, the business rate will be one of the highest in the nation, making Illinois a less competitive state in which to do business.

The new tax plan is intended to be a revenue raiser, originally calculated to be $3.6 billion in the first year — but that was before COVID-19. Yet the fiscal woes facing Illinois are overwhelmingly derived from massive overspending and ballooning pension obligations, and no tax hike will begin to fix it. According to Illinois Policy, the upcoming budget includes nearly $6 billion in deficit spending, with pension costs consuming more than 27% of expected general revenues. Furthermore, Illinois faces a current $4.6 billion shortfall. Without a balanced budget to restrain spending — Illinois has not seen one in 20 years — tax hikes will be inevitable. And by enacting the “fair tax,” Illinois lawmakers have the power of the purse to raise taxes and levy surcharges at their discretion.

According to revised revenue forecasts from the governor’s office, if the fair tax is enacted, the budget gap is approximately $6.2 billion; if the fair tax is not enacted, the estimated budget gap is approximately $7.4 billion. The change from a flat tax to a graduated tax imposed on Illinoisians is simply not worth the $1.2 billion in possible additional revenue when the legislature can’t even be bothered to find a way to cut spending. Governor Pritzker’s attempt to introduce equity in the tax code by making higher earners pay their fair share will hurt all taxpayers and businesses, especially at a time when the effects of COVID-19 on the economy are devastating across the board. The proposed “fair tax” is anything but for the taxpayers of Illinois.

Despite what you may have heard from politicians and journalists, trade deficits are not a bad thing… In fact, they almost always indicate a healthy economy.

Some people (including a number of our civil leaders) believe that the United States’ trade deficit is a bad thing. They think that it means that other countries are abusing us. This is just wrong – and economically ignorant. It is the same as saying that a deficit of sugar in your diet is a bad thing. Just wrong.

By definition, a trade deficit is when one country’s people and businesses are buyingmore goods than they are selling to other countries. Rather than indicating negativity or poverty, this highlights that the people and companies in the United States have the wealth to be able to buy more stuff than the poorer people from other countries are able and willing to buy from us. This is reflective of a healthy economic circumstance. Actually, throughout history when the US has had a trade surplus it generally has been in economic recession or depression. Let’s take a look at what a trade deficit actually is, and why trying to eliminate our trade deficit is misleading and ultimately based in ignorance.

Ultimately, basic economics shows that the amount of money flowing back and forth between two countries has to be the same. What changes is the form of that money: capital vs. consumable goods. When the United States has a trade deficit it means that the United States people and companies as a whole are buying more consumable goods from a country than that country is buying from us. That country in turn is using those dollars to make capital or other investments in the US – rather than buying consumable goods from US companies. China is a great example of this. The reason that we have a trade deficit with China is because we have a lot of wealth and we are willing to spend money on consumable goods. By allowing this deficit, we are in fact just letting Americans enjoy what they want to enjoy, creating a high living standard. The Chinese, on the other hand, are willing to forego the current enjoyment of things so that they can invest in their future – by buying US bonds, or investing in US companies (like automobile plants in Tennessee which provides jobs and economic growth to the US). Those in the US have decided – one by one – that they want to buy stuff to make them happy. Let’s let them do that.

Furthermore, a trade deficit is not a US Government deficit, or debt, or anything of the kind. There is no such thing as a “country’s” deficit. It is not the United States government but rather individual Americans and individual American companies that are choosing to spend their money on consumable goods. The deficit just recognizes that in the moment, US individuals and companies are choosing, transaction by transaction, to part with dollars in exchange for stuff that they would rather have. This is an individual choice that is reflective of individual wealth and ability to spend on consumable goods. We must reject the thinking of some in Congress and elsewhere who are trying to stop US people from buying more stuff from China and other countries. This ignorant recommendation is, by definition, hurting Americans and limiting their freedom to enjoy the things they choose.

An understanding of basic economics shows that trade deficits are a reflection of wealth and success and anyone who denies that doesn’t understand the concepts of trade and deficits.

Everyone is aware of the tragic death of Breonna Taylor and its surrounding circumstances. But many are calling for murder charges against the police officers who did the shooting, and are calling the event evidence of systemic racism. Both positions are ridiculously off base.

The grand jury did not charge any officers with the killing of Ms. Breonna Taylor in her home. The mainstream media would have you believe that this means that the grand jury was derelict in its duties. This skewed, biased view from the media is ignorant of the facts. The evidence clearly delineated that no laws were broken in connection with Ms Taylor’s shooting – the officers were acting within the legal confines of a warrant. The blame for this horrible outcome may well have been that the warrant was issued too easily and with terms that might create an unnecessarily dangerous situation. In fact, none of the actions by the police officers could be counted as homicide or murder nor could they be chalked up to systematic racism. Don’t let the media blind your vision as to where the real injustice is occurring: police warrants.

As Americans who have agreed to live within a republican system of justice, we have no right to contest the grand jury’s decision. However, we do have every right to contest the laws that created this situation. Laws can be flawed and as thoughtful citizens of a republic we have every right to go through the proper channels and request a change of law where we see fit. If the problem is a too aggressive approach by law enforcement, maybe No-Knock warrants should not be allowable, or at least much more restricted. The way to fix the problems that gave rise to the Taylor tragedy is not societal upheaval over racial injustice, as the grand jury found no clear racial motivation involved in the case. No – the answer is criminal law reform, specifically in relation to laws surrounding warrants.

The claim of systemic racism also has no basis. The police entered the home due to a narcotics case with a legally valid warrant to do what was necessary within the home to complete their objectives. The wrongdoing in this case is rather coming from why policemen are busting in in the middle of the night – who gave the order to do that, why is that allowed, and so many other questions that the media should be focusing on. If anyone is really looking to see where the problem was in the Taylor case, it was not the policemen executing a warrant nor the boyfriend who was shooting back in self-defense. Nothing in all this reflects anything about race. The media and demonstrators were charging racism long before the details of the case were known. That alone is clear evidence of the dishonesty of those claiming racism was the cause.

Criminal law reform is where the focus must be if we are actually going to create a better America. Someone’s head should roll. Not the policemen but those who set the dominos in motion. Maybe it’s not a particular person that needs correction but a whole system created by a host of people. The system is the problem. Let’s focus on fixing that.

As Biden is gaining closer to winning the upcoming election, his economic plan deserves more scrutiny. So far, Biden is clearly looking to Obama for his policy aspirations. Unfortunately, Obama was following FDR’s playbook to the detriment of our economy. Let’s take a look:

Obama’s policies resulted in the poorest recovery since the New Deal, just as FDR’s meddling only prolonged America’s longest depression ever. Obama followed FDR’s failed playbook – he raised taxes, over-regulated businesses, gave organized labor excessive power, instituted policies that discouraged people from working, and hurt international trade.

Firmly entrenched in Keynesian economics, Obama believed in government spending while wholeheartedly crowding out private spending; he substituted inefficient political and crony-based spending for free-market, give-the-public-what-they want spending.

This week in the WSJ, Jay Starkman issued a warning on Biden’s plans, in “Bidenomics May Repeat FDR’s Blunder.” He notes, “Today the U.S. economy is recovering from a great crash, as it was before Roosevelt’s tax onslaught. Unfortunately, Mr. Biden doesn’t seem to have learned the right lessons. Should he win in November, he proposes to cancel the Trump tax cuts, raising the top federal income-tax rate back to 39.6%, and raise the corporate income tax from 21% to 28%. He also promises to limit low capital-gains tax rates to the first $1 million in profits and extend the full Social Security tax to income above $400,000.” With Biden also promising to increase regulation and institute energy policy that will produce less energy at a much higher cost, danger is in the wind.

Why go back to the policies that have so clearly failed us before. After three years of robust economic activity during Trump’s administration before the onslaught of COVID, this country can neither risk nor afford Biden’s plans.

Rioting and looting damage society and harm people. The recent protests on behalf of fighting institutional racism wreak with unlawful violence and hypocrisy. Of course there are plenty of peaceful protesters who have caused no physical harm to property or other individuals. These are not at issue. Rather, the focus should be on the 15 people who lost their lives from the initial George Floyd protests, the countless businesses suffering stark physical damage to their properties (and despite ignorant assertions to the contrary, never fully covered by insurance), and the many families who had their livelihoods ripped to shreds because of looting.

The violence that tore through Minneapolis and other cities in recent months is simply never justifiable. The argument made by NPR’s interviewee, Vicky Osterweil, who takes on the Marxist theory that damage to property is neither violent nor unlawful is clearly nonsense. We live in the United States of America, where property and the endangerment of the security of our citizens are imbedded into every page of our Constitution. In fact the Fifth and Fourteenth Amendments delineate this protection of property rights explicitly. Violence to another person’s property is unlawful.

Not only has the recent rioting and looting been unlawful but it has been hypocritical to the highest degree. One mob even attempted to assault Rand Paul and his wife in the name of “social justice.” Disgusting hypocrisy as Rand Paul is the very one who introduced the “Justice for Breonna Taylor Act.” Multiple Americans who died in the Minneapolis riots were minorities. The very Americans – including many of those in racial minorities – whom the violent protestors claim to be protecting were harmed by sky-high property recovery payments and most likely will be faced with spiked insurance premiums in the future. The emotional, physical, and economic freedoms that the rioters and looters claim as their banner are precisely what they themselves are destroying.

If you want to go out and use your freedom of speech in a peaceful way, be my guest– it is your absolute right. If you intend on gathering together a mob full of hatred and hypocrisy, be ready for the consequences. We all ought to be raising our voices against the violent protestors as much as we are trying to solve the civil rights problems of our day. Shame on those who are hypocritically or ignorantly harming the well-being of our own American people.